No matter how often you prefer to monitor your stocks’ performance, there are certain items you should consider. Here are five things to review as you monitor your stocks’ performance:

Earnings — Pay attention to the company’s quarterly and annual earnings statements, which include comparisons with the recent past and often reviews of what management expects for the next quarter and year. Review the stock’s earnings trend and how the company performs compared to analysts’ estimates. Watch out for earnings surprises, which can cause rapid price changes up or down, and may indicate the start of a new stock price trend.

Earnings — Pay attention to the company’s quarterly and annual earnings statements, which include comparisons with the recent past and often reviews of what management expects for the next quarter and year. Review the stock’s earnings trend and how the company performs compared to analysts’ estimates. Watch out for earnings surprises, which can cause rapid price changes up or down, and may indicate the start of a new stock price trend.

Price and dividends — Follow

Price and dividends — Follow

the stock’s price compared to its

52-week highs and lows. Examine its trailing total returns year to date and over the last one-, three-, five-, and 10-year periods. Look for changes in the absolute dollar amount of dividends and the current yield (the annual dividend divided by the current price).

P/E and PEG ratios — Price to earnings (P/E) and price/earnings growth (PEG) ratios are often better indicators than the stock price as to how relatively expensive or cheap a stock is.

P/E and PEG ratios — Price to earnings (P/E) and price/earnings growth (PEG) ratios are often better indicators than the stock price as to how relatively expensive or cheap a stock is.

The P/E ratio is useful for comparison to other stocks and the market, while the PEG ratio is a strong indicator of whether the stock is overpriced or underpriced compared to its projected earnings growth rate over the next five years.

Insider transactions and stock

Insider transactions and stock

buybacks — A company buying

back its own stock or whose senior

executives and directors are accumulating more shares is a bullish sign.

On the other hand, when insiders are selling off major holdings of their own stock, it’s quite often an indication that the stock price has peaked.

Sudden and large price changes

Sudden and large price changes

on high volume — When a stock

makes a sudden, high-volume move

— particularly when it opens much

higher or lower than the previous day’s high or low — it can be the start of a new, long-term trend.

For help monitoring your stocks’ performance, or if you need to make a change to your investment portfolio, please call.

I f you are new to investing, there is no doubt that you will make some mistakes; it just goes with the territory. However, you should familiarize yourself with these common mistakes and take steps to avoid them.

No Investment Plan — Many investors just get started in the stock market without giving any thought as to what they are trying to accomplish. It is important to have a plan that will keep you on track and help you ride out turbulent markets. Your plan should include:

Goals — Define what you are

trying to accomplish so you

can measure your portfolio’s performance in meeting your goals. You will want to be as specific as possible,

such as accumulating $1 million for retirement by age 60 or $100,000 for your child’s education within 15 years.

Risk Tolerance — Define how much risk you are comfortable with so you can determine an appropriate allocation for your assets. Stocks are riskier than bonds and will fluctuate more than other asset classes, so you want to figure out how much risk you are willing to assume. The younger you are, the more risk you can typically assume,

since you have more time to overcome any declines in your investments.

Asset Allocation — You will want to determine how to allocate your assets across different investments, such as stocks, bonds, etc.

Diversification — Once you determine your asset allocation, you will want to diversify within each individual asset class. For example, when investing in stocks, you will want to spread your funds across large-, mid-, and smallcap stocks.

Time Horizon — Don’t wait too long to start investing because time is your friend. If you

are saving for retirement, plan on 30 years of investing to meet your goals. If you don’t allocate enough time to meet a specific goal, you will need to adjust your asset allocation

to help you meet the goal within a shorter timeframe. For example, if you start saving for a child’s college education when he/she is a

freshman in high school, your assets will most likely need to be allocated more heavily to stocks in an attempt to meet that timeframe.

Stop the Noise — Be careful

with how much time you spend and

the credence you lend to the financial

media. Media noise can be hard

to turn off, but remember the best

advice is to stick to your plan.

Not Rebalancing — You will want to review your portfolio regularly and rebalance if it strays from your target asset allocation. When

you allow your portfolio to drift based on market returns, some asset classes will be overweighted at market peaks and underweighted at market lows, which may lead to poor performance. While it will sometimes feel counterintuitive to sell assets that are performing well for those that are not performing as well, your target asset allocation

will lead to a stronger performance in the long term.

Chasing Performance — Many investors are always trying to find the next big investment. They will rely on recent strong performance

Chasing Performance — Many investors are always trying to find the next big investment. They will rely on recent strong performance

as the single factor in purchasing an investment. If a certain stock has been doing extremely well for a number of years, you should probably have invested in it years ago,

since it may be nearing the end of its high performing cycle.

When an investment is doing extremely well, many people will not sell and take the profit because they are afraid that it will continue

to increase in value. But there is also the risk that it will go down in value.

You should also consider identifying a target value at which you will sell your stocks. This will help take the emotion out of your sell

decisions.

Becoming Too Emotional — It’s hard not to get emotional when the market encounters a severe correction, but the investors who have

the ability to remain calm during these times more consistently outperform the market. If you start selling off investments at the worst

possible time, you may then be out of the market when it starts to rebound.

While it is easier said than done, you have to build a resistance to those things that create emotional triggers so you don’t make bad

decisions. Thoughtfully consider new information, don’t just follow the crowd, and make decisions when you are calm based on your long-term plan.

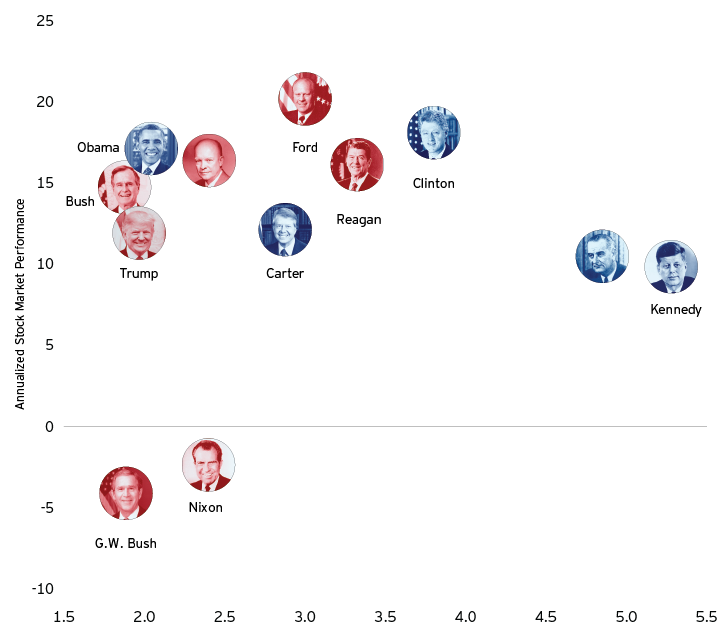

Politics and investing have always been spoken about in the same breath. Commentators and candidates alike often frame the performance of the stock market as a sort of “barometer” of a president’s policies. But the data don’t support this link. Over the past 120 years, the long-term performance of the market has shown almost no correlation with government policies.

So what’s the real story when it comes to politics and investing?

Consider these historical truths:

Neither party can lay claim to superior economic or financial market performance. The S&P 500 Index delivered an average annual return of approximately 11% over the past 75 years, through both Democratic and Republican administrations. The US economy also expanded around 3.0% during that period.1

Presidential term stock market return vs. economic growth (1957-present)

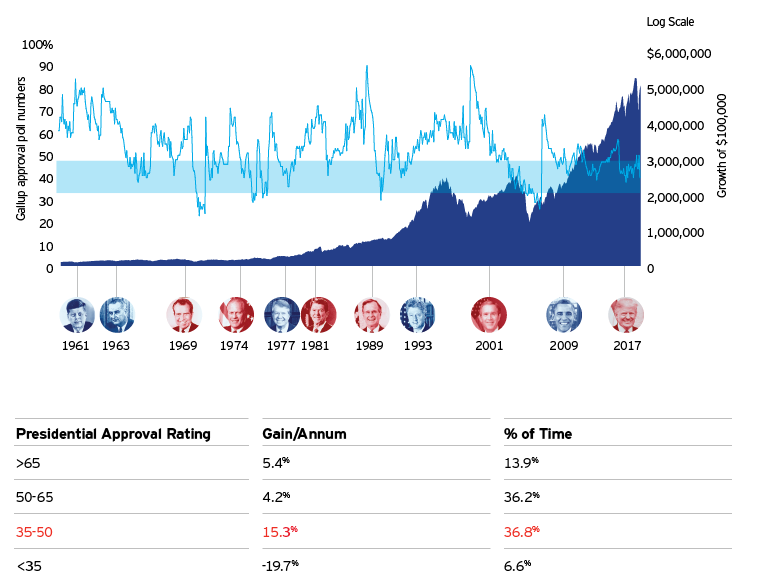

From the inauguration of President Kennedy through the current administration of President Trump, some of the best returns in the stock market have come when the president’s approval rating was between 36% and 50% — in other words, when at least half the country disapproved of the job performance of the sitting president.2

Gallup poll presidential approval ratings and the growth of $100,000

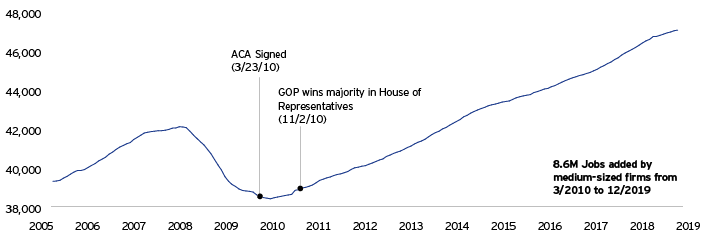

Predictions about the ultimate impact of legislation are often far removed from the actual results. For instance, it was predicted that President Obama’s Patient Protection and Affordable Care Act of 2010 would destroy small-business hiring. But since it was implemented, 8.6 million jobs have been added in this sector.3 Similarly, President Trump’s Tax Cut and Jobs Act of 2017 was intended to unlock capital expenditures, but it has thus far failed to bring an acceleration in business investment as issues such as trade uncertainty and, most recently, Coronavirus have impacted confidence.

Example 1: Patient Protection and Affordable Care Act

Employers with 50 or more full-time employees are considered “large business” and therefore required to offer employee health coverage or pay a penalty.

Non-farm private medium payroll employment (50-499)

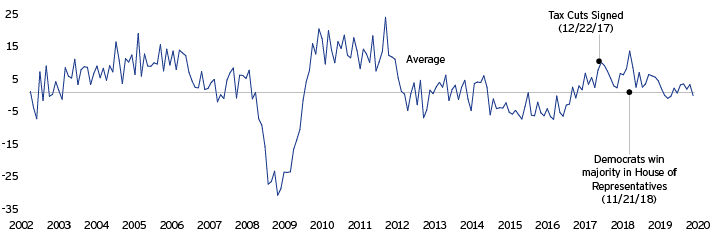

Example 2: Tax Cuts and Jobs Act of 2017

Section 179 allows taxpayers to deduct the cost of certain property (such as machinery and equipment purchased for use in trade or business) as an expense when property is placed in service.

US capital goods new orders (nondefense ex-aircraft and parts)

These are just some of the essential truths about elections and investing. Click here to see a brochure which clearly and simply illustrates these three, plus seven more:

Spring is a good time to clean out the cobwebs, and not just in your home or apartment. Your personal finances can benefit from a good spring cleaning, too. Here are some questions to ask yourself regarding your budget, debt, and taxes.

A budget is the centerpiece of any good personal financial plan. After tallying your monthly income and expenses, you hopefully have money left over to save. But… is there room to save even more? Review your budget again with a fine-tooth comb to see if you might be able to save an additional $25, $50, $100, or $200 per month. Small amounts can add up over time. If you participate in a workplace retirement plan, you might not even notice your slightly smaller paycheck after you increase your contribution amount.

If your expenses are running neck and neck with your income, try to cut back on discretionary spending. If that’s not enough, look for ways to lower your fixed costs or explore ways to increase your current income. Budgeting software and/or smartphone apps can help you analyze your spending patterns and track your savings progress.

When it comes to your personal finances, reducing debt should always be a priority. Whether you have debt from student loans, credit cards, auto loans, or a mortgage, have a plan to pay down your debt as quickly as possible. Here are some tips.

Spring also means the end of the tax filing season. You might ask yourself the following questions:

This communication is strictly intended for individuals residing in the state(s) of CO, CT, FL, NJ, NY, NC, OH, PA and RI. No offers may be made or accepted from any resident outside the specific states referenced.

Prepared by Broadridge Advisor Solutions Copyright 2020.